- 17 Oct, 2023

Understanding the Loan-to-Value Ratio for Home Equity Loans without Appraisal

The reality of no appraisal home equity loan

You have been that proud homeowner for all these years and invested a lot in improving the value of your home! All of us do it because our homes are our favorite place, isn’t it? And now you are in need of some extra funds. You will have your own reasons, be it for some more home improvement, debt consolidation, investing in education, or covering medical expenses. What options do you have to get your funds?

Well, the solution seems obvious. You go for a “home equity loan” where the funds can be borrowed against your home’s equity. Most homeowners prefer to get a home equity loan due to its flexibility feature. However, one major downside is that the appraisal process takes a lot of time while you apply for a home equity loan. Although there are ways to skip the appraisal process and get funds faster.

In this blog, we will shine a light on the reality of no appraisal home equity loan. In addition to this, we will learn the significance of the loan-to-value ratio and the home equity loan requirements.

Home equity loan basics

Hello my mortgage friends, understanding the fundamentals of home equity loans is highly important. A home equity loan can be viewed as a second mortgage that helps homeowners access funds by securing their home equity.

Home equity is the difference between the market value of your home and the outstanding balance you owe on your mortgage. For instance, if the value of your home is $200,000 and you owe $150,000, your equity would be $50,000. Let’s have a brief look into the common uses of home equity:

-

Home improvements

Many individuals who want to make new additions and improve the comfort of their homes, go for home equity loans to fund these renovation projects.

-

Debt consolidation

Those who want to get off the stress of debt mountains, make good use of a home equity loan to pay off their high-interest debts.

-

Education expenses

The funds drawn from home equity can be used for paying your or your child’s tuition fee and other education expenses.

-

Medical & emergency expenses

Homeowners who want to cover unexpected expenses for medical or any urgent repairs also utilize a home equity loan.

No appraisal home equity loans - Explained

To be honest, you don’t get to completely skip the appraisal process. A home equity loan no appraisal essentially means that you will not be going through the traditional appraisal process, but instead, lenders rely on automated valuation methods (AVMs) or real estate market data to estimate your property's value.

-

The reason for the popularity of home equity loans with no appraisal is their speedy approval process.

-

It offers convenience to borrowers who have an immediate requirement of funds. However, you need to have a strong financial portfolio in order to be eligible for a home equity loan with no appraisal.

-

Traditional appraisal is the process where a professional appraiser inspects your home to determine the actual value compared to other homes in the same locality.

The reality of no appraisal home equity loan

As attractive as it sounds, the no appraisal option comes with some drawbacks that can make the acquisition process a bit challenging. Let’s what the real world no appraisal looks like by addressing the potential benefits and challenges:

| Benefits | Challenges |

|---|---|

| 1) A home equity loan no appraisal skips the most time consuming step of scheduling an appraiser, waiting for their available time, and the final appraisal report. So, funds can be accessed faster. | 1) The loan amount offered might not meet the homeowner’s expectations as the valuation relies on automated methods and current market data which in turn results in a not-so-accurate estimate. |

| 2) The appraisal process is not done for free. There is an appraisal fee that the homeowner is requested to pay. The cost differs depending on the complexity of the evaluation. | 2) In order to mitigate the risk, lenders charge higher interest rates than those for traditional home equity loans. |

| 3) Those individuals who are completely confident regarding their property’s value will be able to access funds by establishing a strong home equity. They need to worry about disapproval. | 3) As the real estate market keeps fluctuating for every quarter of a year, property values will go up and down. So, avoiding the traditional appraisal process results in impacting the real value of the home. |

What is LTV and how is it determined?

LTV ratio plays a crucial role in determining the lender’s risk. It showcases the relationship between the loan amount that the borrower requires and the appraised value of the property. As the borrower’s LTV ratio increases, the risk for lenders also goes up and they end up charging a higher rate of interest. In addition to that borrowers are also expected to purchase private mortgage insurance in order to mitigate the lender’s risk. Two essential factors that determine the loan-to-value ratio are:

-

Loan amount - This amount signifies the required funds that a borrower is willing to take out from the lender. In the case of a home equity loan, if you require funds of around $45,000, this would be the loan amount.

-

Property value - The value of your property is determined not just by the looks of it. It is the appraised value of the property that we discussed in the above sections.

These two are the prime factors used to calculate the LTV ratio. For example - If your loan amount is $90,000 and the appraised value is $150,000, your LTV ratio is 60%. [Mortgage amount divided by appraised value and multiplied by 100 = LTV ratio]

If your LTV ratio is below 80% you are on the safe side of the island. Anything more than 80% is considered a higher ratio and you as a borrower will have to face higher borrowing costs and purchase private mortgage insurance.

If you have a higher LTV, try increasing your down payment. For instance, if your loan amount is $90,000 and you make a down payment of $15,000, your loan amount will be reduced to $75,000 ultimately reducing your LTV ratio.

LTV for Home Equity Loans without Appraisal

By now you would have gained the importance of loan-to-value ratio while requesting funds from lenders. If you want to enjoy lower interest rates and get 100% approval, it is important to have a lower LTV ratio.

-

If you skip your appraisal, you might increase your LTV ratio because the appraised value might be inaccurate due to prevailing market conditions and automated systems used. It is important to understand that a loan-to-value ratio can make or break your application.

-

There can be chances of application denial in case of a higher LTV ratio. So, it is advised to get a property appraisal done for your property in order to secure a lower loan-to-value ratio.

3 Must-Have Home equity loan requirements

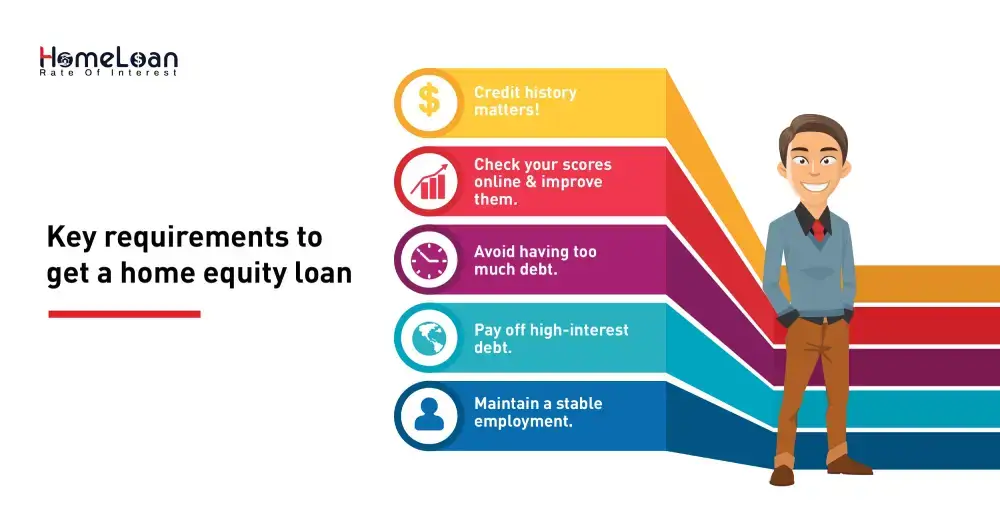

Once you have decided to make good use of the funds you get from your home’s equity, it is essential to understand the requirements and be prepared with an application that the lenders can not even think of rejecting. Meeting these requirements is not just necessary but beneficial for the borrower to secure the best interest rates and loan terms.

-

Credit score and history

We can’t judge a book by its cover but in the world of lending, a lender can judge your creditworthiness by your credit history and the score. This includes your payment history, frequency of credit purchases, repayments, and other revolving debts that will influence your interest rates and loan terms. You can utilize the credit report tools online to predetermine how much you score.

-

Debt to income ratio

This highlights your ability to handle debt on top of the current income that you have. Lenders will assess if you can handle additional debt from the home equity loan. A DTI of 36% and lower is commonly preferred by lenders. If you have a higher DTI, make sure that you reduce it by paying off existing debts or high interest credit applications.

-

Employment & income status

Your employment type affects the income you receive on a regular basis. It is necessary to show stable proof of income to the lenders to showcase that you can successfully repay the loan. You will be requested to submit proof of income documents such as your pay stubs, tax returns, and bank statements. If you’re self-employed, you may need to provide additional documentation to verify your income.

We all know that the current market conditions will see fluctuations as the year progresses. It is a common phenomenon that occurs every single week. So, the interest rates, housing market conditions, people’s lifestyles, and living conditions change according to the overall market condition.

Every individual will have their own needs to get a home equity loan. Going for the appraisal or skipping the whole process highly depends on their personal circumstances and the need for funds. We recommend that you go for a home equity loan with no appraisal only after careful research and consideration of the benefits and challenges.

Get in touch with a mortgage professional who can assist you with adequate information regarding home equity loans without an appraisal. We at HLRI, aim to align your home equity loan funds with the main goal. If you would like to get more awareness about no appraisal home equity loans, visit our blogs and you will get a clear understanding.